Caird Investment Partners, LLC ("Caird") is a SEC-registered investment adviser focused on regulated financial institutions. We advise banks on liquid TLB portfolio management, securities portfolio strategy, and broader balance sheet optimization. We also originate and underwrite bilateral and private credit transactions.

Q1 earnings landed into one of the more dislocated macro environments in recent memory. The Iran conflict, a contentious and uncertain Fed leadership transition, and the compounding effects of tariff policy hit simultaneously. Combine this with the existing and continued market concerns on the medium/long-term impact of AI on business models. Conventional frameworks were not built for moments with this many variables in flux at the same time. The practitioners navigating it best are not waiting for clarity; they are asking better questions. That is the lens for this issue.

The Caird Team

From the Caird Team

The Risk That Markets Kept Repricing Away

The Strait of Hormuz carries roughly 20% of the world's seaborne oil. In March, flows through it dropped from more than 20 million barrels per day to roughly 3.8 million. The IEA called it the largest supply disruption in the history of the global oil market. Brent crude surged more than 55% from pre-conflict levels, touching $120 at its peak.

The more interesting observation is not the spike itself. It is how many times markets repriced the risk down in the weeks before it materialized. Ceasefire signals, diplomatic gestures, and temporary pauses each produced sharp oil pullbacks. Each pullback was treated as a resolution. Very few portfolios were structured around the scenario that actually unfolded: a partial, unstable re-opening with the U.S. Navy blockading Iranian ports and Iran controlling Hormuz traffic. As of late April, Brent settled above $118. Infrastructure damage to Qatar's Ras Laffan LNG complex alone carries a three to five-year repair timeline.

The structural changes running underneath are less visible but more durable. Dollar hegemony in energy markets is being stress-tested in ways that outlast any ceasefire. Saudi Arabia has expanded yuan-denominated oil settlement with China, and the volume of non-dollar energy invoicing has grown materially since the conflict escalated. These are not temporary accommodations. They reflect a reorientation of global buyer-seller relationships that took decades to build and decades more of stability. Now, given an acute macro shock, these relationships are rapidly shifting structure which in turn will take time to truly understand the second-order impacts. Even a full cessation of hostilities does not reset the clock. Naval mine clearance in the Strait alone is estimated to take up to six months once active conflict ends, meaning physical supply normalization trails any diplomatic resolution by a significant margin.

There is a pattern here worth naming. Markets are very good at pricing the modal outcome. They are structurally inclined to reprice tail risks down each time a resolution appears possible. The investors and institutions that manage through these periods best are not the ones who called the scenario correctly. They are the ones who nimbly adjusted their probability of each scenario and adjusted their portfolio accordingly.

For portfolio management and asset allocation, the question is practical: how exposed are you to a persistent energy shock and potential stagflation, and is that exposure explicit or embedded? Some of it is obvious, airlines, where fuel runs 25 to 30% of operating costs, and shipping/logistics companies that may not be able to pass on higher fuel costs. Some are less visible: packaging companies where petroleum-derived resin inputs reprice quietly, specialty chemical producers whose feedstock costs are directly oil-linked but rarely headline the investment thesis, and building materials manufacturers (insulation, adhesives, coatings) where the petroleum exposure is embedded several layers deep. The earnings calls this quarter are starting to surface the information needed.

Market Signals

Widening

CLO Spreads: Supply Pressure Building

March CLO issuance down 43% YoY; warehouses ramping

March CLO issuance dropped to 67 deals totaling $27.6 billion, down 43% from March 2025. The pullback reflects macro uncertainty and loan market bifurcation, not a lack of structural demand. Datapoints that generally point to future issuance remain robust; warehouse pipeline data indicates this is more a pause with volume to follow, than a real slowing in volume. Reset volumes are likely to contribute to a pick-up in volumes too, as call protection rolls off deals priced over the last few years. When those managers come to market, AAA spreads are likely to widen further.

For bank securities portfolios, the current moment is one of patience. CLO AAA spreads have moved from roughly 110 bps pre-Liberation Day to 125–130 bps on new issue. Sophisticated buyers are watching the pipeline and positioning to deploy when spread levels more fully reflect the overhang. Strong credit enhancement and favorable capital treatment make the asset class worth the wait.

Active

TLB Earnings: What the Data Is Showing

Dispersion accelerating across sectors and geographies

We track earnings across a portfolio of 300+ internally underwritten public and private TLBs across a range of industries and geographies. A few patterns from Q1: infrastructure and recurring-revenue services held up well, as did aerospace and defense. AI-enabled software is separating from AI-adjacent storytelling; the market is pricing the difference and TLB prices reflect it. Electronic market-making had a standout quarter. Consumer discretionary was mixed, with softness in outdoor recreation and auto retail offset by strength in experiential leisure. Geography continues to matter; sector-level results can mask significant regional dispersion underneath.

Watch

NDFI Lender Finance: Stress Surfacing

Redemption pressure and competitive dynamics shifting

Private credit firms are leaning into CLO securitization amid redemption pressure and terms are softening. We are seeing creative transactions from non-BSL CLO managers to refinance their liabilities in non-traditional ways. Banks with NDFI relationships should be reviewing attachment points and concentration. The simultaneous push by large financial institutions into private credit changes the competitive dynamic in ways that are not yet fully priced. Fee income and balance sheet relationships built during the expansion deserve a fresh look.

Stress

Private Credit: Redemption Pressure Building

Record $19.5B in Q1 withdrawal requests; several managers gating

Investors sought to withdraw a record $19.5 billion from private credit/direct lending funds in Q1 2026, citing growing credit quality concerns. Several of the largest managers in the $1.8 trillion market have exercised gates to block redemptions, an unprecedented step that signals the liquidity mismatch embedded in the asset class is no longer theoretical. As liquidity demands ramp up against portfolios of illiquid/semi-liquid assets, will redemptions outpace inflows in both magnitude and duration such that assets need to be aggressively sold? Caird leans no, but we also advise a framework of preparing for that opportunity if it presents itself.

By the Numbers

~43%

Decline in CLO new issue deal count (LevFin Insights)

March 2025 to March 2026: 106 deals / $48.2B vs. 67 deals / $27.6B. Supply expected to accelerate as warehouses ramp.

13%

Bank securities unrealized losses as a % of Tier 1 capital (Bankview USA)

Down from a $700B peak in 2022–2023. At current book yields for many bank portfolios, recovery still takes years, not quarters.

$114

Brent crude per barrel, late April 2026 close (Bloomberg)

Up from ~$72 pre-conflict. Shut-in of wells will take years for output to fully recover.

~$1.1T

U.S. bank loans outstanding to NDFIs, Q1 2025 (Federal Reserve)

Up from ~$350B in 2015. Stripping NDFI growth from C&I data shows small and mid-size bank lending essentially flat.

Three Things We Are Talking About

01

THE FED WITH WARSH AT THE HELM

Warsh cleared the Banking Committee on a party-line vote, a first in the committee's history. He is expected to favor rate cuts, and President Trump has consistently pushed for them. But the FOMC is not a rubber stamp: Cleveland, Minneapolis, and Dallas all declined to support an easing bias at the April meeting, and inflation is moving in the wrong direction led by energy. The market's assumption that Warsh equals cuts is probably too simple. Warsh has a stated preference against monetary policy implementation using non-rate mechanisms. Should we expect rate cuts alongside accelerated MBS portfolio runoff? Or, while out of consensus, sales of Treasury bonds? What matters more is how he handles a divided committee navigating a genuine inflation shock. Portfolio managers are right to hope for clarity before acting, but we believe the right framework is identifying the tails and getting ahead of potential market responses to clarity when it arrives.

02

IS THE AGGREGATE CONSUMER CREDIT DATA LYING TO YOU?

The headline delinquency rate on consumer loans at commercial banks sits at 2.62%, manageable by historical standards. However, the average is hiding serious stress: delinquency in the lowest-income ZIP codes has moved above 20%, while higher-income cohorts remain relatively stable. The median VantageScore declined for the first time in years in Q4 2025, and more consumers are drifting toward the highest and lowest risk tiers simultaneously, a distribution that aggregate data obscures entirely. Additionally, the March FRBNY Survey of Consumer Expectations shows that 9.1% of respondents now expect to be 'much worse' off a year from now, a level of pessimism that significantly outstrips the peak of the pandemic and has only been surpassed twice since 2013: during the Russia-Ukraine invasion and the 2025 tariff concerns.

03

IS THE 2021–2022 VINTAGE PROBLEM ARRIVING NOW?

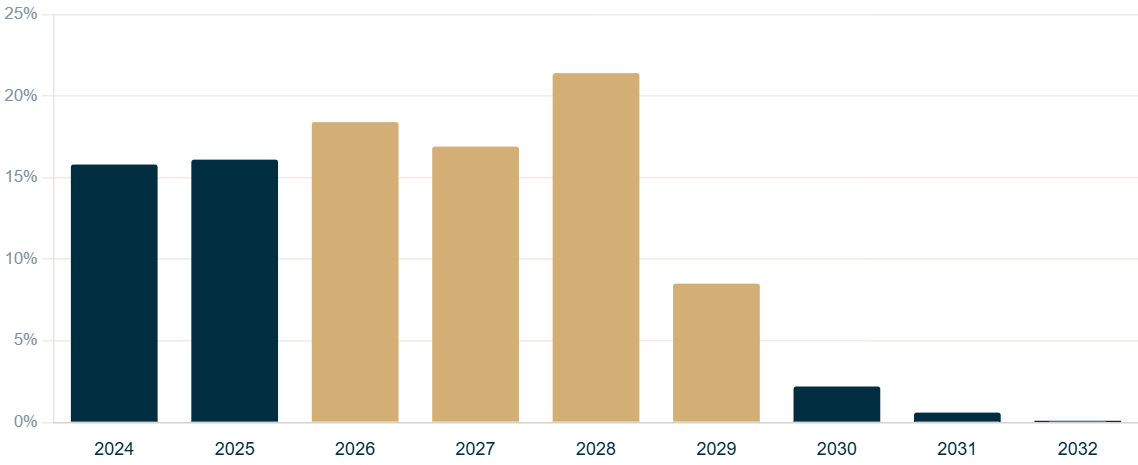

Loans underwritten at peak multiples in 2021–2022 are entering their stress window. The leveraged loan distress ratio climbed to 7.23% at the end of March, a three-year high and up from 4.34% in December 2025. An LCD survey in March found 92% of market professionals expect default levels to increase at least slightly over the next six months, a sharp deterioration from 67% in December. Software and healthcare are the most concentrated sectors in liability management activity. The broad default rate understates the problem. Based on the chart below from the Fed and after adding in 12 to 18 months for covenant relief/flexibility/amend-and-extend/PIK periods, 2025 was the beginning and 2026–2029 is the real window.

Maturity Wall in Private Credit

Share of loans (by dollar value) maturing by year

What We Are Hearing From Our Clients

Three Conversations from April

“The traditional C&I playbook is getting crowded.”

Competition for core C&I credits is intense and pricing reflects it. The banks making meaningful progress are expanding sourcing into adjacent channels: liquid TLA/TLB portfolios, specialty verticals like ABL, equipment finance, and healthcare lending, and bilateral direct lending transactions that carry C&I balance sheet classification but originate through distinct relationships. The question we hear most is not whether to expand; it is which of these channels fits the institution's risk appetite and existing team. What peers are doing varies more than most bank executives realize.

“We keep hearing about TLBs. What does it actually take to do this right?”

The interest is real and the use case is intuitive: liquid assets that can scale up or down as the broader balance sheet requires, with C&I classification and yield that competes with traditional origination. What banks are working through is the execution question.

Some are sizing the opportunity and benchmarking what peers carry as a percentage of total assets. Others already have a portfolio but it is small, concentrated, or not actively managed. The more important question is whether the exposure is being managed with the discipline the market demands. CLO managers, hedge funds, and dedicated credit platforms are the dominant participants in this market. They run full underwriting teams, have real-time pricing, and operate with information advantages that compound over time. Banks entering this market benefit most when they have access to equivalent credit infrastructure, whether built internally or through a dedicated adviser.

The fiduciary question is equally important. Caird operates as a fiduciary to our bank clients, and we believe that alignment between adviser and client is foundational for regulated institutions.

Looking forward, the institutions that will benefit from the current dislocation the most are those that are proactive. Spread widening and market volatility creates real buying opportunities, but only for managers who have already done the underwriting work. You cannot build a list of names the day the market moves. The banks that have invested in the infrastructure now, whether internally or through a dedicated adviser, will be positioned to deploy when the opportunity is clearest.

“Pressure on private credit. What does that mean for us?”

The increasing focus on performance within private credit, coupled with more conservative back-leverage pricing and advance rates, has naturally narrowed the bandwidth for new originations in that space. This creates an opening for thoughtful lenders to be front-footed in the middle market. As competition for deal flow shifts, regional banks with established C&I and leveraged lending capabilities are well-positioned to re-engage with borrowers seeking stable alternatives. With current pressure on both timing and pricing, there is a timely opportunity to capture quality transactions that may have been out of reach just two years ago.

Chart of the Month

The headline spread numbers for agency MBS do not fully capture the cost of the borrower's prepayment option, a form of negative convexity driven by prepayments eroding realized yields. A metric that truly encompasses the value of the option sold, and the negative convexity sold alongside, is OAS (Option Adjusted Spread). CLO AAA bonds offer floating rate exposure, the same 20% risk weighting, and spreads that have consistently run well above an accurate measure of agency MBS spreads.

The Caird Perspective

What Q1 Earnings Are Telling Us: Origination Can't Outrun Payoffs

Regional bank Q1 results were broadly strong. Net income growth exceeded expectations across most of the sector, driven by expansion in both net interest and noninterest income, and several banks revised full-year NII guidance upward. Fixed-rate asset repricing continued its work, credit quality held up well, and for an industry that absorbed significant stress in 2023, the recovery in earnings power is real.

The more interesting question is what the next chapter looks like.

Loan growth is the central tension. Pipelines are healthy, origination volumes came in at or above plan at most institutions, and C&I production is broadly accelerating. But net loan balances are not keeping pace. Payoff volumes ran well above expectations across the sector, borrowers refinancing into markets offering terms regional banks structurally cannot match, or simply taking advantage of favorable exit conditions. Compounding this, multiple management teams called out large regional banks returning aggressively to the C&I market, competing at sub-200 basis point spreads with weakened covenant structures. Banks choosing not to match those terms are losing volume today to preserve credit discipline tomorrow. The production is there. The balance sheet doesn't yet show it, and that gap is unlikely to fully close before 2027.

Capital is in a strong position and the NIM story is real, but the composition is shifting. The deposit cost tailwind is nearly exhausted; multiple CFOs said as much directly, with further improvement contingent on Fed action most banks are no longer modeling. What remains is fixed-rate asset repricing as legacy loans roll to current market rates. The banks beginning to separate are those building differentiated earning asset channels alongside it: specialty C&I verticals, liquid TLB portfolios, and securities book discipline that generates additional yield without extending duration. The Q1 numbers reward that posture. So will Q2.

Caird Team Update

Year One.

This month marks Caird's one-year anniversary. What started as a conversation about what banks actually need from an advisor has grown into something we are genuinely proud of. Thank you to our clients, partners, the broader community, and most importantly, our families that have supported us. We are just getting started.

Where We Have Been and Where We Are Headed

The Caird team is headed to the TBA Annual Convention in Dallas, May 20–22, and to Chicago for client meetings. We would love to connect.

From the Team: As penalty for finishing last in the Caird Inaugural Masters Pool, Ben Marshall was in full caddie attire for the team's golf outing (including the bib) and was required to read any putt upon request. He accepted this with remarkable grace (picture below).

After a similarly spirited NCAA bracket competition, Matt finished last. Per the terms, he will deliver a three-minute address to the team recounting his failures as a bracket strategist and will be running a race with us in a 30-pound weighted vest. We will report back in June.