Q4 2025 FDIC Quarterly Banking Profile

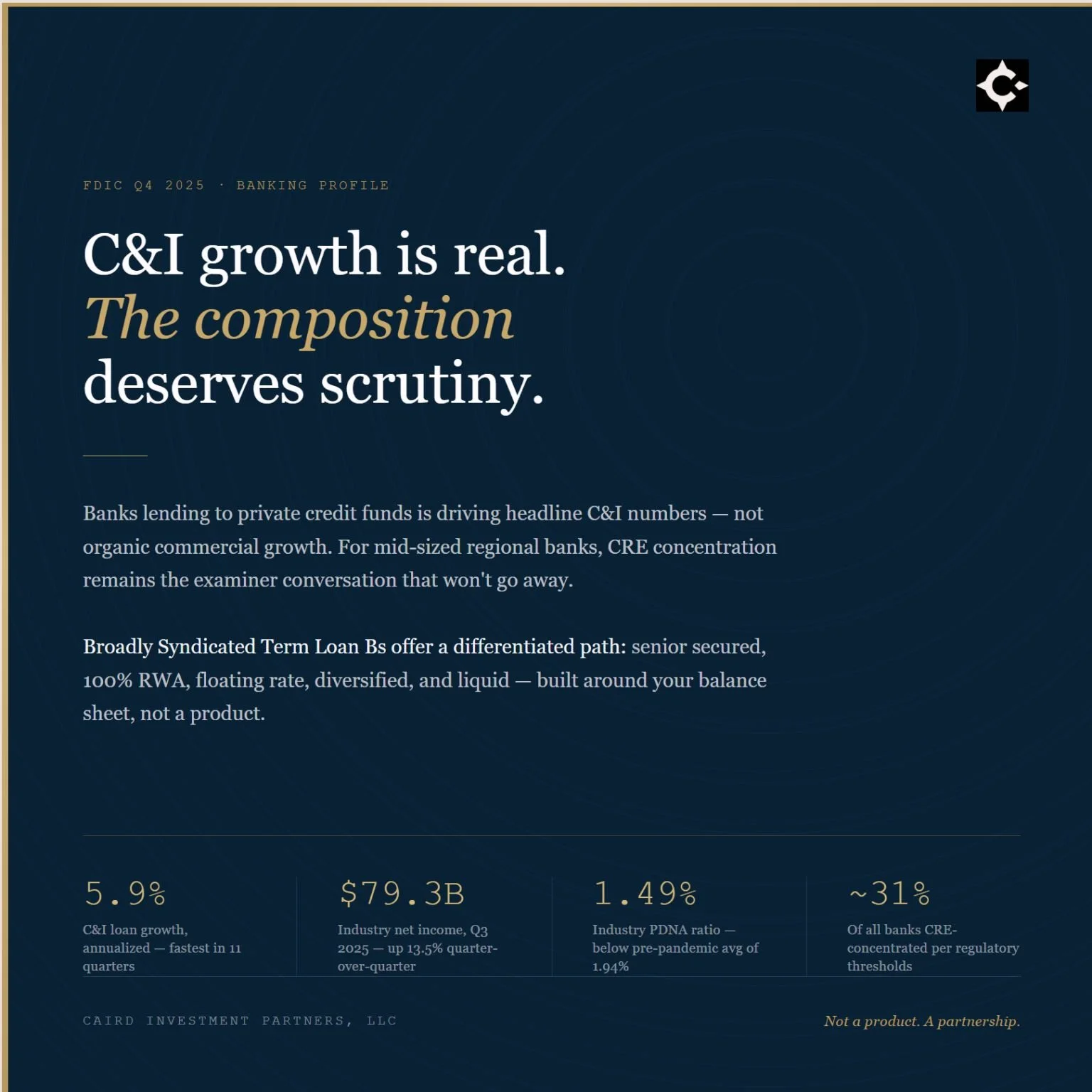

The Federal Deposit Insurance Corporation (FDIC)'s Q4 2025 Quarterly Banking Profile headlines strong C&I loan growth, 5.9% annualized, the fastest pace in 11 quarters. Look closer and the picture is more nuanced.

A meaningful portion of that C&I growth is coming from loans to non-depository financial institutions. Essentially, banks lending to private credit funds. At the same time, scrutiny on private credit portfolio marks is intensifying, particularly around software and software-adjacent borrowers where valuations have come under pressure.

For mid-sized regional banks $10B–$100B, the more pressing issue may be a familiar one: CRE concentration. Not CRE stress, most banks are managing that, but the concentration itself. Regulators and examiners are asking harder questions about the share of capital tied to a single asset class, regardless of performance.

Broadly Syndicated Term Loan Bs offer a differentiated path to C&I growth, senior secured, 20% RWA, floating rate, diversified across industries, and without the concentration dynamics that define both CRE-heavy and NDFI-exposed portfolios. Most importantly, these loans are liquid meaning a portfolio can be optimized over time and scaled up and down based on a bank's core needs.

One focus at Caird Investment Partners, LLC is helping banks build bespoke TLB strategies around their specific balance sheet needs. Not a product. A partnership.